Managing NSW Deposit Limits and Cash Flow

Jul 07, 2026

Introduction

This Strategic Navigator has been developed by AMEC COLLEGE® as a practical companion resource for our NSW Licensed Builders CPD Courses. It expands on the compliance, contractual, and financial management principles covered throughout our CPD program, helping builders understand how NSW deposit limits, cash flow management, Home Building Compensation (HBC) requirements, and compliant payment practices work together to reduce business risk.

While our CPD courses focus on meeting the continuing professional development requirements for licensed builders in NSW, this guide provides additional practical strategies, checklists, and real-world guidance that can be applied immediately to improve compliance, protect cash flow, and support better project outcomes.

Learn more about our CPD Club for NSW-licensed builders.

Strategic Navigator

Managing NSW Deposit Limits and Cash Flow

(2025/2026)

1- Executive Context

1- Executive Context

The Shifting Landscape of Residential Liquidity

In this climate, your deposit isn't just a down payment; it's your project's life support. In the 2025/2026 NSW regulatory environment, the management of project liquidity has evolved from a back-office task into a high-stakes survival exercise. While deposit limits are marketed as consumer protection, they serve as the financial foundation of your build. Mastering these limits is a strategic necessity for maintaining solvency. If you get the numbers wrong, you aren't just facing a fine; you're handing a weapon to the homeowner to use against you in the NSW Civil and Administrative Tribunal (NCAT).

The Home Building Act 1989 exists to balance homeowner security with builder risk, but for the builder, it is a minefield of potential non-compliance. This document bridges the gap between strict legal precision and the pragmatic "boots-on-ground" reality of running a construction business. We are moving past administrative box-ticking; we are building a shield to protect your commercial interests. To survive, you must understand the legal thresholds that dictate your initial cash position before the first shovel hits the dirt.

2- The 2025/2026 Regulatory Matrix

10% vs. 5% Thresholds

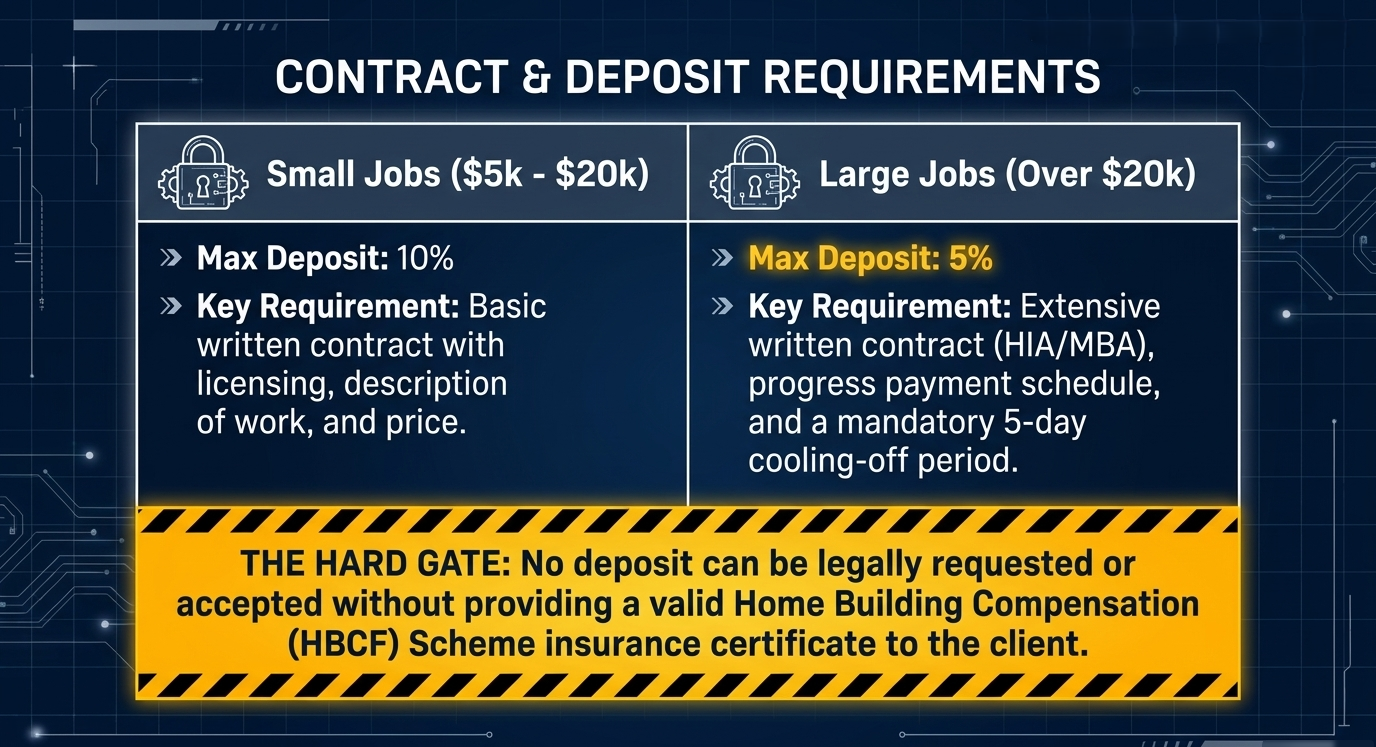

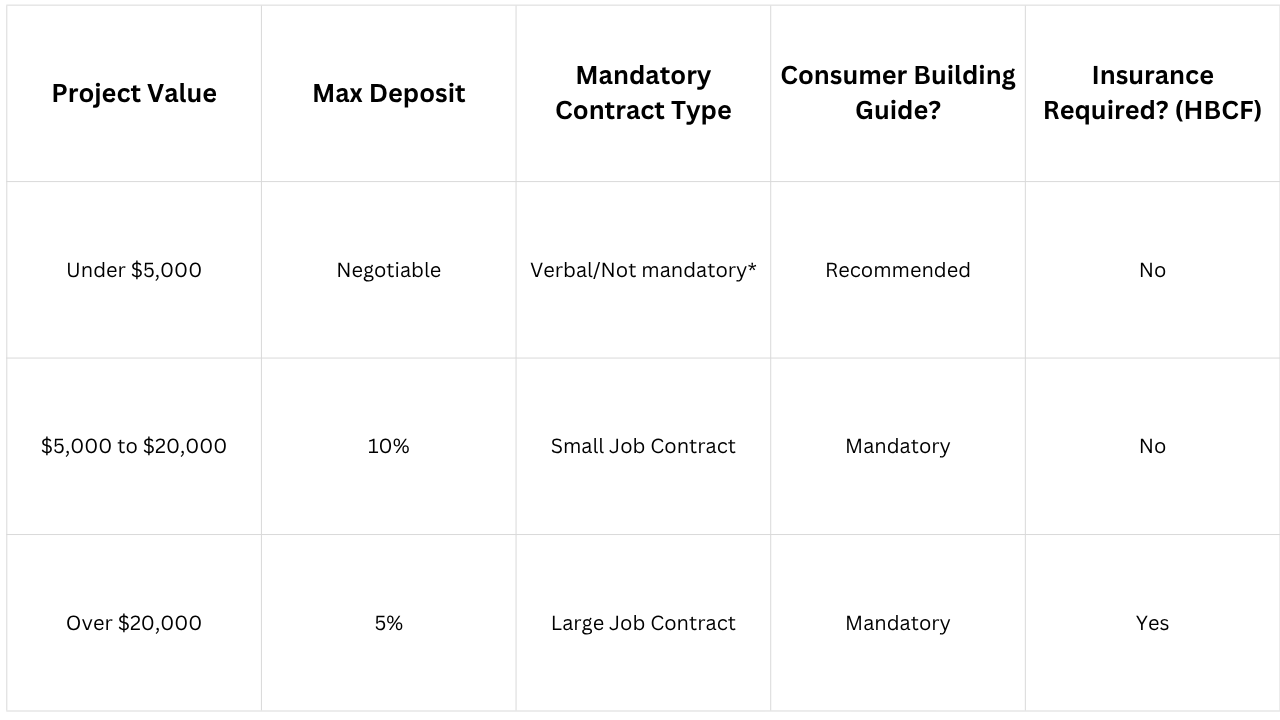

Miscalculating the contract price isn't a "rookie mistake"; it’s a corporate liability. Under the current framework, an incorrect deposit request can trigger penalties up to $110,000 for corporations. The legality of your deposit is dictated by the total contract value, and the regulator has a very low tolerance for "rounding up."

The $20,000 mark is your critical pivot point. For projects exceeding this value, your deposit is legally capped at 5%. This is designed to mitigate risk for the consumer, but for you, it means your cash flow must be engineered elsewhere. Furthermore, you must remember the $5,000 threshold: a written contract is mandatory for everything over $5,000, and you must provide the Consumer Building Guide for every job in this bracket. Failing to do so is a common point of failure that gives owners an easy "out" in a dispute.

NSW Deposit Limit Matrix (2025/2026 Guidelines)

*Note: Even if not mandatory, the MBA veteran’s advice is simple: if it’s not in writing, you don’t have a leg to stand on in NCAT

3- The HBCF Insurance Hurdle

The "No Certificate, No Cash" Rule

For projects over $20,000, the deposit is legally "locked" behind the Home Building Compensation (HBC) Scheme. For a builder, the speed of securing this insurance directly dictates your project’s velocity.

It is a criminal offence to request or receive any payment, including the deposit, before providing the homeowner with a valid Certificate of Cover. Taking a client's cash without the certificate in their hand is the fastest way to lose your license and face prosecution.

Builder’s Pre-Invoice Verification Checklist:

- ☐ Verify Contract Value: Confirm if the total project (including GST) exceeds $20,000.

- ☐ Secure HBCF Cover: Apply for the Certificate of Cover immediately upon contract signing.

- ☐ Provide the Certificate: Physically or digitally deliver the certificate to the homeowner.

- ☐ HBC Check: Use the official portal to ensure the certificate is active and reflects the correct project details.

- ☐ Issue Deposit Invoice: Only now is it legal to ask for the 5%.

4- Strategic Playbook

How Builders Can "Not Get Stuck"

The primary fear is that a 5% deposit on a large project won't cover your initial site establishment and material outlays. Hope is not a strategy. The solution lies in your Progress Payment Architecture. You must shift focus from the deposit to the rapid achievement of the first major milestone.

Methods for Maintaining Cash Flow

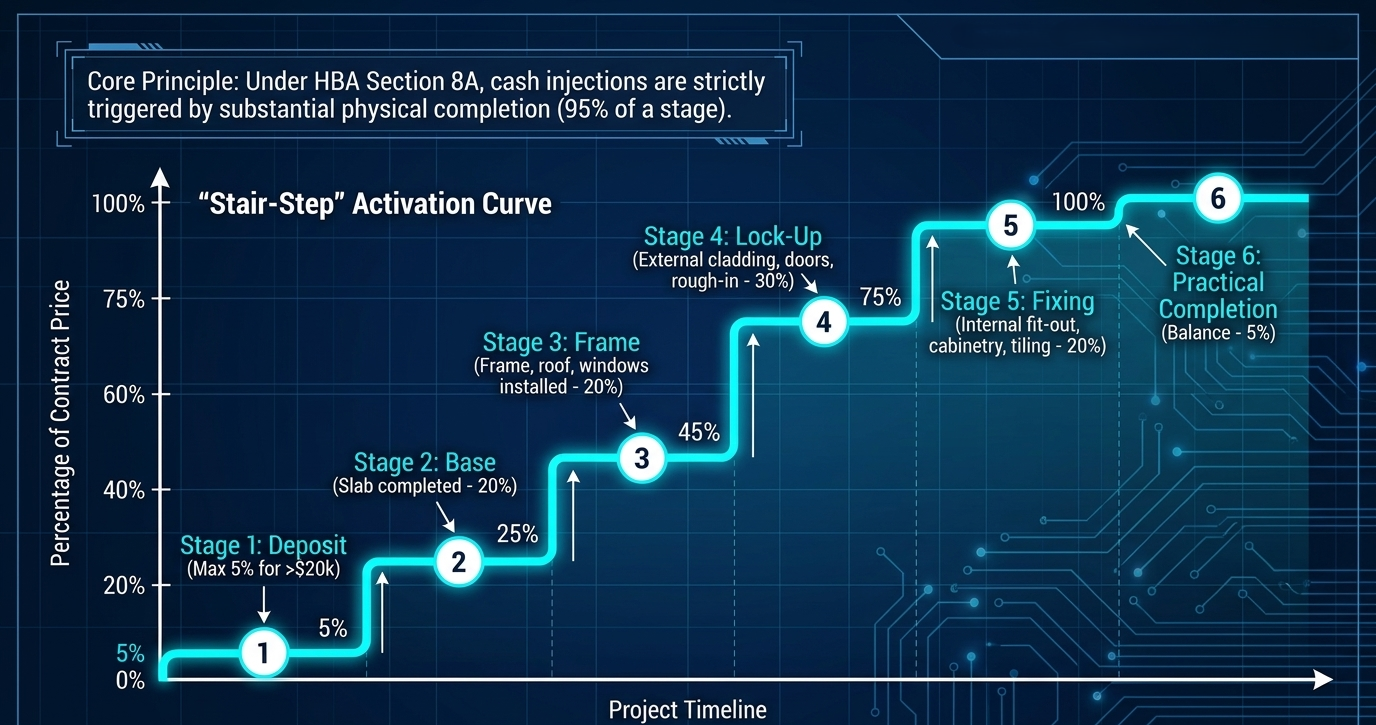

- Milestone Realignment (The "Base" Stage Strategy): Standard HIA/MBA milestone structures (Base, Frame, Lock-up) are your starting point, but the Schedule of Values must be front-loaded to the maximum legal limit. Ensure all legitimate "Site Establishment" costs, fencing, site toilet, sediment control, and initial plant hire are captured within the "Base" claim. You aren't "front-loading" (which is illegal); you are ensuring the claim accurately reflects work actually done to trigger that 15-20% payment as fast as possible.

- Itemised Specification Control: Vague specifications trap your capital. Listing brand and model for every fixture prevents "Prime Cost" (PC) and "Provisional Sum" (PS) blowouts. Every PC item is a variable that can fluctuate and freeze your margin. Lock in detailed specifications to minimise these entries.

- The Variation Trap and SOPA: If a variation isn't signed, it’s a gift to the homeowner. Every change must be documented, signed, and paid for before the work starts. Under the Security of Payment Act (SOPA), your rights to claim for variations depend on following the written protocols.

- The 10-Day Rule: Once you submit a payment claim under SOPA, the client has a 10-business-day window to provide a payment schedule. If they miss this, they are legally liable for the full amount. Never let a variation "wait until the end."

5- Red Flag Analysis

Avoiding Non-Compliant Payment Structures

"Front-loading", asking for money for work not yet performed, is a massive liability in NCAT. It creates a "non-compliance liability" that a savvy homeowner will use to freeze your payments mid-build.

Risk vs. Reality: Payment Warning Signs

- Excessive Deposits (15-20%): On a $20k+ project, this is a statutory breach. It’s an immediate red flag for regulators.

- Vague "Acceleration" Clauses: Avoid custom clauses demanding 30% at slab stage without physical work to justify it.

- Text Message Variations: Texting is for "coffee is on the way," not for changing a kitchen layout. If it isn't a signed variation document, you are funding the client’s whims out of your own pocket.

Lump Sum vs. Cost-Plus

- Lump Sum (Fixed Price): The preferred protection for builders seeking predictable margins.

- Cost-Plus Warning: Per HIA guidelines, Cost-Plus should generally be reserved for projects over $1 million or genuine "unknowables" (heritage restorations). Using Cost-Plus for a standard $600k new build makes you a compliance target for regulators. It requires forensic record-keeping; NCAT will disallow claims for personal vehicle expenses or office overheads every time if they are wrongly charged.

6- Final Directive

Professional Best Practices for 2026

Transparency isn't just about being a "nice guy"; it’s a professional defence. A builder who follows the 5%/10% rule and provides the Consumer Building Guide up-front builds a "reputational asset." When you end up in a dispute (and you will), being the party that followed the law makes you the party that gets paid.

The Builder’s Survival Actions:

- NEVER take a cent without HBCF cover: For any job over $20,000, it is a criminal offence to take money before the certificate is issued.

- MANDATE the Consumer Building Guide: Provide it for every job over $5,000. No excuses.

- ALIGN payments to physical milestones: Trigger the "Base" stage fast by capturing site establishment costs legally.

- DOCUMENT and PRE-PAY variations: Link them to your SOPA rights. If it’s not signed, don't pick up the tools.

- KILL the PC/PS Items: Use detailed specifications to lock in fixed prices and protect your cash flow.

Compliance is not an administrative burden; it is a sophisticated tool for risk management. Use it to ensure your business is still standing in 2027.